Johann Sebastian Bach, the great German composer and musician, once said

“I was obliged to be industrious. Whoever is equally industrious will succeed equally well.”

Johann Sebastian Bach

Bach was a prolific artist. He composed more than a 1,000 original pieces, over a 40 year period. In fact, he kept composing music right up to his death, in 1750 AD. I don’t know of many musicians today who can boast of such a feat.

Even though popular perception has it that when producing creative work, one cannot substitute quantity for quality, I have read in a number of places that authors, musician, painters work diligently everyday…. many a time working at the same time & place… almost like going to office daily. They all acknowledge the fact that a stroke of genius doesn’t happen by accident but by purposeful work. In this regard, Bach was no different. He had a very regimented approach to composing his music, diligently spending time each day doing what he loved most. He knew he had to put in the hours to compete with contemporary composers such as Vivaldi, Telemann & Handel. And above all else, he was German, so, peristent work came naturally to him.

As kids, I am sure that each one of us has been told the Aesop’s fable of “The Grasshopper and the Ant”…. about how the industrious Ant gathered food for the winter while the lazy Grasshopper whiled away the summer only to die of starvation in the winter. This was supposed to teach us that doing something was somehow better than doing nothing.

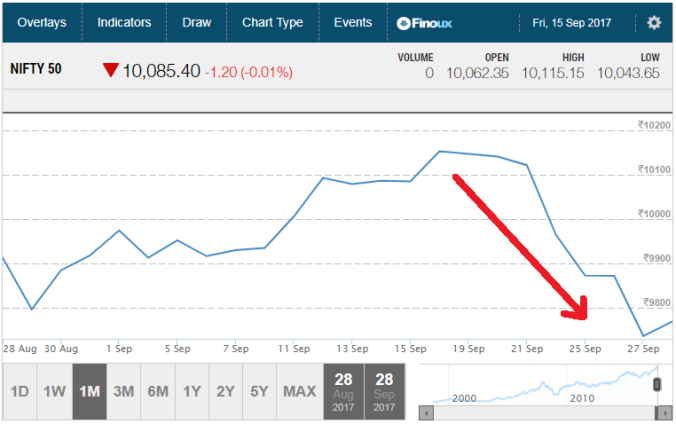

I am sure that this advice of being industrious is applicable to most aspects of life but for one, Investing. Nifty 50, over the past week has had a few vicious sessions, falling from a peak of ~10,150 to ~9,730 which represents a fall of almost 5% in the space of a couple of sessions.

The fall has been much worse for the Nifty Next 50, Midcap and Smallcap indices. When there is so much volatility, especially on the downside, there is a tremendous urge to do something. Behavioral finance has taught us that the pain we feel when $1 is lost is only offset by $2 of gains. This is called “loss aversion”. So, per unit, loss hurts more than the happiness gain gives. Thus, many a time, people tend to panic when they see a ⇓ or a red number in their portfolio. They feel the urge to do something to stem the loss. Typically, they end up selling. Is this the right strategy?

Empirical studies have clearly proven that one cannot time the market…. So, when you sell something, you never know if the trend will reverse the next day or the next year. And when it does reverse, you don’t know whether to buy again or wait… fearing another correction. This is a slippery slope…. timing the market never has worked. If it had, you would see billionaire technical analysts whose sole business it is to time the market.

Jack Bolge, one of my heroes, had this to say when he was asked what an individual investor had to do when the Dow Jones Industrial Index had suffered a few brutal sessions of selling.

“Don’t just do something, stand there!”

Applied to Investing, this is Jack’s take on the famous American adage “Don’t just stand there, do something!”

Watch the full video by clicking below…. don’t miss it….. absolute 100% gold.

https://finance.yahoo.com/video/individual-investors-stay-course-bogle-180600539.html?format=embed

Dragging one’s feet might not be a bad strategy in investing. The only people who make money when we keep “doing something” are the brokers. So, sloth, one of the 7 deadly sins, is not at all bad when it comes to investing. All one has to do is to ignore the temporary losses as if nothing has happened. This is easier said than done though.

I am going to do absolutely nothing if the Nifty 50 falls another 10% or 20% or 30%. I am going to keep investing as long as I have cash coming in. I have developed a thick skin when it comes to losses. Knowing the history of the financial markets, I know for sure that I will be rewarded handsomely for doing nothing. Contrary to what Bach said, equally industrious investors won’t succeed equally well. Perhaps Investing is the only place where you get paid better when you do nothing.

So, the next time the market goes bonkers, and you have an urge to do something… Remember Jack Bogle’s immortal words, “Don’t just do something, stand there!”

Read the disclaimer here.